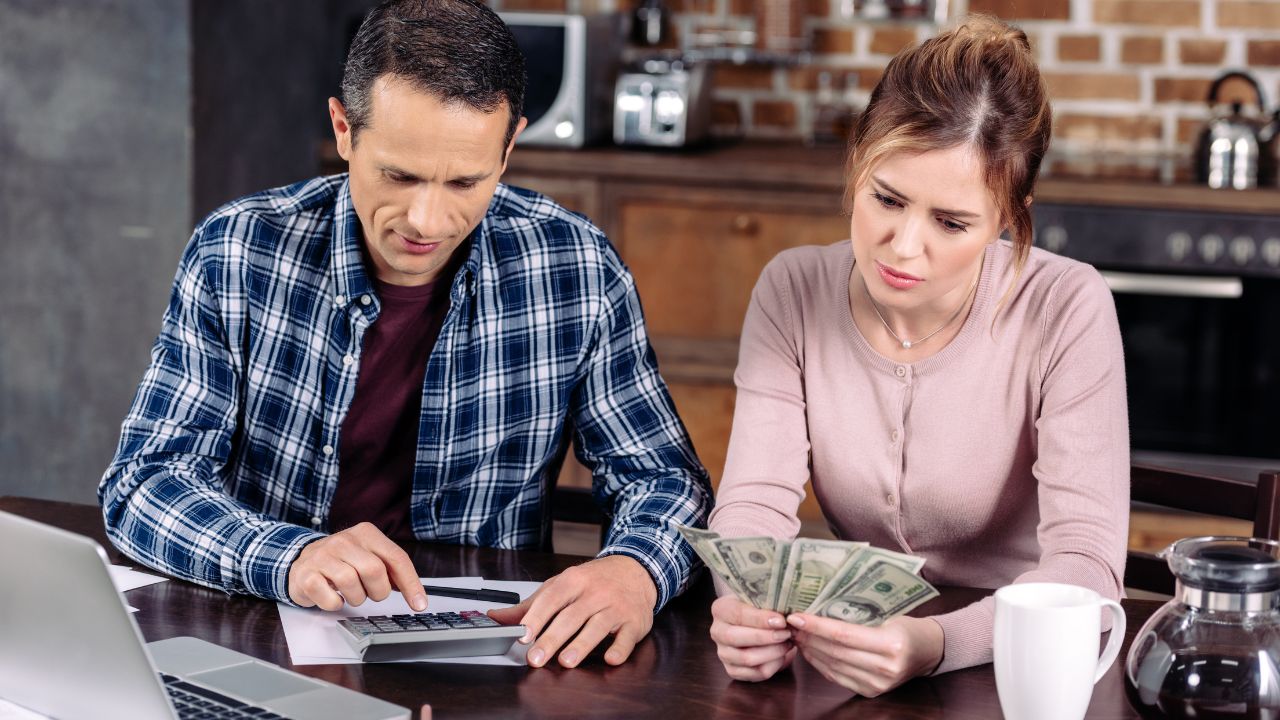

13 Money Mistakes Californians Regret Making in Their 40s

Your 40s are a strange financial decade. You’re not new to money anymore, but you’re not done building either.

Income is often higher, responsibilities are heavier, and retirement suddenly starts feeling closer.

This is also the decade where a lot of people look financially confident on the outside and quietly say, “I should’ve handled that differently” on the inside.

These are the money mistakes many Californians regret making in their 40s, along with why they matter more than they seem at the time.

Pausing Retirement Contributions “Just for a While”

One of the most common regrets sounds harmless at first. Pausing retirement savings temporarily.

People stop or reduce contributions to handle a tight stretch, a renovation, tuition, or lifestyle upgrades. The plan is to restart soon.

Sometimes soon turns into years.

Your 40s are prime compounding years. Money invested has time and momentum on its side. Missing even a few years can create a noticeable gap later.

Here’s a simple example.

Say someone invests $600 per month starting at age 40 and earns an average 7 percent annual return. If they keep contributing for 25 years, they end up with roughly $455,000.

Now change one detail. They pause contributions for just five years and start at age 45 instead, still investing $600 per month at that same return. After 20 years, they end up with about $315,000.

That “short break” cost about $140,000 in future retirement money.

Many people say they didn’t realize how expensive that pause would become until they ran the numbers later.

Compounding doesn’t just reward consistency. It quietly punishes interruptions, too.

Letting Lifestyle Inflation Eat Every Raise

Income often rises during your 40s. So do expenses, but not always for unavoidable reasons.

Bigger house. Nicer cars. More subscriptions. More dining out. More everything.

Each upgrade feels reasonable on its own. Together, they quietly absorb every raise.

Years later, people realize their earnings grew but their investing didn’t.

Comfort is good. Automatic spending creep isn’t.

Carrying High Interest Debt Too Long

Credit card balances and personal loans sometimes linger through one’s 40s longer than expected.

With higher income, it feels manageable month to month.

The problem is that the interest keeps working full-time even when you’re not thinking about it.

Many people regret not attacking high-interest debt more aggressively when their earnings were strong enough to do it faster.

Interest is patient. It waits and compounds.

Not Increasing Investments With Income

A lot of workers set their retirement contribution percentage early and forget to revisit it.

If you started at 6 percent in your 20s or 30s and never increased it, your savings rate may no longer match your earning power.

Your 40s often bring your highest earning years. That makes them your strongest investing years too.

People often wish they had bumped contributions with every raise instead of leaving them frozen in time.

Set it and forget it works better for slow cookers than savings rates.

Ignoring a Written Financial Plan

Many people in their 40s operate without a real written plan. They save some, invest some, spend the rest, and hope the math works out.

Without a plan, it’s easy to drift.

Goals stay vague. Timelines stay fuzzy. Tradeoffs stay unexamined.

Later regret often sounds like this: “We earned good money. We just didn’t manage it the best.”

A written plan turns motion into direction.

Underestimating College and Education Costs

Parents often underestimate how fast education costs grow.

By the time kids reach their late teens, tuition numbers can feel shocking.

Some families rely too heavily on loans or last-minute scrambling because early planning didn’t happen.

Many say they wish they had started dedicated education savings earlier or more consistently, even in smaller amounts.

Time helps education savings almost as much as retirement savings.

Not Building a True Emergency Fund

In your 40s, your financial life gets more complex. More bills. More dependents. More things that can break.

Some households still operate without a solid emergency fund, relying on credit instead.

That works until it doesn’t.

Job loss, medical issues, or major repairs hit harder when there’s no cash buffer. Regret usually shows up after the first big surprise.

Emergency funds feel optional right up until they’re essential.

Delaying Insurance Reviews

Insurance decisions made in your 20s and 30s often stay untouched for too long.

Life insurance, disability coverage, home coverage, and umbrella policies may no longer match your real-life situation.

Your income is higher, your assets are larger, and dependents may rely on you more.

People often regret not reviewing and updating coverage sooner, especially after a major life event.

Old policies don’t automatically grow with new responsibilities.

Co-Signing Loans Without a Backup Plan

Helping family feels right. Co-signing sometimes feels like the fastest way to do it.

But when payments get missed, the co-signer owns the problem. Credit damage and repayment responsibility shift quickly and legally.

Many people in their 40s say they underestimated this risk when helping friends or relatives.

Generosity is good. Open-ended liability isn’t.

Investing Too Conservatively Out of Fear

After living through market downturns, some investors in their 40s shift too heavily into ultra-safe assets too early.

Safety feels comforting, but portfolios still need growth at this stage.

Retirement may still be 20 or more years away.

People often regret being too cautious for too long and missing years of market recovery and growth.

Risk in one’s 40s is usually best when it’s managed, not eliminated.

Putting Estate Planning Off Again and Again

Estate planning sounds like something for “later” until later gets close.

Wills, beneficiary designations, healthcare directives, and powers of attorney often get delayed through the 40s because life feels busy and the topic feels uncomfortable.

Many families later wish these documents had been completed earlier and updated regularly.

Planning ahead is a gift to the people you love, not a pessimistic act.

Not Talking About Money With a Partner

Some couples avoid detailed money conversations for years.

Accounts stay separate without strategy, goals stay assumed instead of discussed, and one partner handles everything while the other stays in the dark.

In hindsight, people often regret not creating shared visibility and shared planning earlier.

Assuming There’s Plenty of Time to Fix It Later

This is the most common regret sentence of all for people entering their 50s.

“I thought I had more time.”

Your 40s feel busy and midstream, but they’re also a financial turning point. Decisions here carry more weight because the runway, while still long, is no longer endless.

The good news is awareness beats perfection. Most money mistakes are fixable once they’re visible.

The earlier you spot them, the cheaper they are to correct.

16 Things Every American Kitchen Had in 1975

Step into an American kitchen in 1975, and you’d find the same comforting sights and sounds no matter where you were.

It wasn’t fancy, but sometimes we wish we could go back to those days.

16 Things Every American Kitchen Had in 1975

9 Iconic Candies That Ruled 1970s Corner Stores

The 1970s were a golden time for candy lovers. Whether you were sneaking sweets into class or swapping treats on the school bus, certain candies were just part of growing up.

If you remember unwrapping a treat while watching The Brady Bunch, this one’s for you.